Mutual Fund Taxation in India

Published: 17 Jul 2026

Mutual fund taxation can feel stressful for new investors. You may not know how much tax you need to pay after selling your units. Different tax rules can make the process even more confusing. You may also worry about making a mistake while filing your tax return. These problems can reduce your confidence as an investor. A clear understanding of the rules can help you avoid such issues.

1. What is Mutual Fund Taxation?

Mutual fund taxation means the tax you may pay on the profit earned from your investment. Tax usually applies when you sell or redeem your mutual fund units at a profit. The tax amount depends on the type of mutual fund you own. Equity funds and debt funds may follow different tax rules. Your holding period also decides whether the gain is short-term or long-term. Dividend income from mutual funds may also be taxable. Understanding these rules can help you plan better and avoid unexpected tax costs.

2. When Do You Pay Tax on Mutual Funds?

You may need to pay tax when you sell or redeem mutual fund units at a profit. This profit is called a capital gain. You do not usually pay capital gains tax only because the value of your investment has increased. Tax normally arises when you sell the units and receive the profit. You may also pay tax when a mutual fund gives you dividend income. Switching money from one mutual fund scheme to another can also create a taxable gain.

3. Important Mutual Fund Tax Terms

Before learning mutual fund taxation, you should understand a few basic terms. These terms help you calculate tax and understand how much profit you have earned.

1. Capital Gain

A capital gain is the profit you earn after selling your mutual fund units. For example, you invest ₹50,000 and later sell the units for ₹60,000. Your capital gain is ₹10,000. Tax may apply to this profit, not to the full selling amount.

2. Capital Loss

A capital loss happens when you sell your mutual fund units for less than the purchase amount. For example, you invest ₹50,000 but sell the units for ₹45,000. In this case, your capital loss is ₹5,000. You may use an eligible capital loss to reduce tax on other capital gains.

3. Holding Period

The holding period is the time between the purchase date and the sale date of your mutual fund units. It helps decide whether your profit is short-term or long-term. Different types of mutual funds may have different holding-period rules.

4. Short-Term Capital Gain

A short-term capital gain is the profit earned after holding mutual fund units for a shorter period. The exact holding period depends on the type of fund. Short-term gains may have a different tax rate than long-term gains.

5. Long-Term Capital Gain

A long-term capital gain is the profit earned after holding mutual fund units for a longer period. Long-term gains may receive different tax treatment. Investors should check the latest rules before selling their units.

6. Equity Mutual Fund

An equity mutual fund mainly invests money in company shares. Large-cap, mid-cap, small-cap, and equity index funds are common examples. These funds usually follow equity mutual fund tax rules.

7. Non-Equity Mutual Fund

A non-equity mutual fund mainly invests in assets other than company shares. It may invest in bonds, gold, international shares, or other mutual funds. debt funds, gold funds, and some hybrid funds can fall into this category. Their tax rules may depend on the fund type and purchase date.

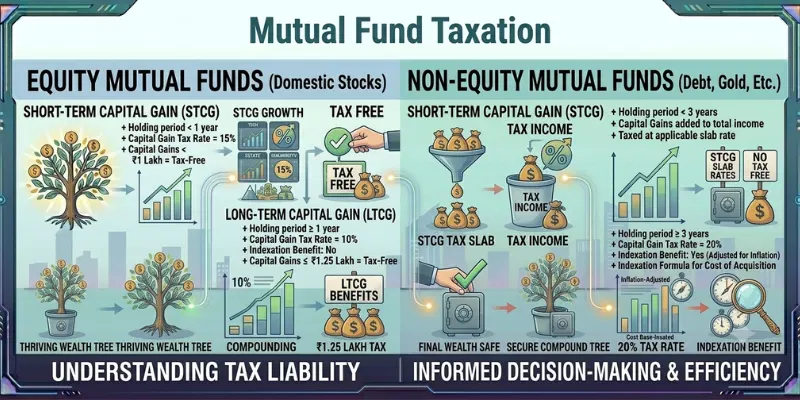

4. Taxation of Equity Mutual Funds

equity mutual funds mainly invest money in the shares of Indian companies. Large-cap, mid-cap, small-cap, flexi-cap, elss, and many Indian equity index funds fall into this group. For tax purposes, a scheme generally needs to invest at least 65% of its assets in the equity shares of domestic companies. However, some fund-of-funds schemes may not receive equity tax treatment, even when they invest in other equity funds. Always check the scheme’s official tax category before calculating tax.

1. Short-Term Capital Gains Tax

Your profit is called a short-term capital gain, or STCG, when you sell equity mutual fund units within 12 months of purchase. For transfers made on or after July 23, 2024, this profit is taxed at 20%. Surcharge and a 4% health and education cess may also apply.

For example, suppose you invest ₹1,00,000 in an equity fund and sell it after eight months for ₹1,30,000. Your short-term profit is ₹30,000. The basic tax at 20% will be ₹6,000. Cess and any applicable surcharge will increase the final amount slightly.

2. Long-Term Capital Gains Tax

Your profit becomes a long-term capital gain, or LTCG, when you hold equity mutual fund units for more than 12 months. Long-term gains of up to ₹1.25 lakh in one financial year are exempt under the applicable rule. Gains above this combined annual limit are taxed at 12.5%, without indexation.

This ₹1.25 lakh limit is not separate for every mutual fund. It generally applies to the total eligible long-term gains from equity mutual funds, listed equity shares, and other assets covered by the same tax section during the financial year.

For example, imagine you invest ₹3,00,000 and sell the units after two years for ₹4,60,000. Your long-term gain is ₹1,60,000. After using the ₹1.25 lakh exemption, the taxable gain will be ₹35,000. The basic tax at 12.5% will be ₹4,375. Cess may also apply.

3. Securities Transaction Tax

Securities Transaction Tax, or STT, is a small tax charged on eligible equity transactions. The special 20% STCG and 12.5% LTCG rates generally require STT to be paid on the eligible equity mutual fund transaction. The fund house or exchange usually handles this charge, so investors do not normally pay it separately through their income tax return.

4. Important Points to Remember

Every sip instalment has its own purchase date. This means one instalment may qualify as a long-term investment, while a newer instalment may remain short-term. A switch from one equity scheme to another also counts as a redemption. Therefore, it may create a taxable capital gain. You should check the purchase date, sale date, total gain, and remaining annual exemption before redeeming your units.

5. Taxation of Debt and Hybrid Mutual Funds

Debt and hybrid mutual funds do not always follow the same tax rules as equity funds. Their tax treatment depends on where the fund invests its money, when you purchased the units, and how long you held them. Therefore, investors should check the fund category before calculating tax.

1. Taxation of Debt Mutual Funds

debt mutual funds mainly invest in fixed-income options. These include government securities, corporate bonds, treasury bills, and money market instruments. They usually carry lower market risk than equity funds, but they are not completely risk-free.

a. Debt Funds Purchased on or After April 1, 2023

Gains from specified debt mutual funds purchased on or after April 1, 2023, are generally treated as short-term capital gains. This rule can apply even when you hold the investment for several years.

A specified mutual fund generally means a fund that invests more than 65% of its money in debt and money market instruments. It can also include a fund that invests at least 65% in units of such a debt fund. This updated definition applies from April 1, 2026.

The gain is added to your total taxable income. You then pay tax according to your applicable income tax slab. You do not receive an indexation benefit under this rule.

b. Example of Debt Fund Taxation

Suppose you invest ₹2,00,000 in a debt mutual fund after April 1, 2023. You sell it later for ₹2,40,000. Your capital gain is ₹40,000.

This ₹40,000 may be added to your taxable income. Your tax will depend on your income tax slab. For example, a person in the 20% tax slab may pay ₹8,000 as basic tax, excluding cess and surcharge.

c. Debt Funds Purchased Before April 1, 2023

Older debt fund investments may follow different rules. The holding period and redemption date can affect their taxation. Long-term gains on eligible older investments are generally taxed under the current long-term capital gains rules.

The tax treatment can become complex because the rules have changed over time. Investors should check the exact purchase date before selling older debt fund units.

2. Taxation of Hybrid Mutual Funds

Hybrid mutual funds invest in both equity shares and debt instruments. However, all hybrid funds do not follow one tax rule. The fund’s equity and debt allocation decides its tax category.

a. Equity-Oriented Hybrid Funds

A hybrid fund may receive equity tax treatment when it meets the required domestic equity investment level. Aggressive hybrid funds and some arbitrage funds may fall into this category.

When you sell units within 12 months, the gain is short-term. It is generally taxed at 20%.

When you sell units after more than 12 months, the gain is long-term. Eligible long-term gains of up to ₹1.25 lakh in a financial year are exempt. Gains above this limit are generally taxed at 12.5%.

b. Debt-Oriented Hybrid Funds

Some hybrid funds invest most of their money in debt instruments. Conservative hybrid funds may fall into this group.

When a fund invests more than 65% in debt and money market instruments, it may come under the specified mutual fund rules. Gains from eligible units purchased on or after April 1, 2023, may be treated as short-term gains and taxed according to the investor’s income tax slab.

c. Other Hybrid Funds

Some hybrid funds may invest between 35% and 65% in domestic equity. These funds may not qualify as equity-oriented funds or specified debt mutual funds.

For such funds, the gain may become long-term when the required holding period is completed. Long-term gains are generally taxed at 12.5% without indexation. Short-term gains are usually added to taxable income and taxed according to the investor’s slab rate.

d. Example of Hybrid Fund Taxation

Suppose Priya invests ₹1,50,000 in an equity-oriented hybrid fund. She sells it after 15 months for ₹1,90,000. Her long-term capital gain is ₹40,000.

When her total eligible equity long-term gains remain within the annual ₹1.25 lakh exemption, she may not pay LTCG tax on this gain. However, the result can change when she has other eligible gains during the same financial year.

e. Important Tip

Do not judge a hybrid fund only by its name. Two hybrid funds may follow different tax rules because their equity and debt allocations are different. Check the scheme document or capital gains statement before filing your tax return.

6. Common Mutual Fund Tax Mistakes

- Treating all mutual funds the same: Equity, debt, and hybrid funds may follow different tax rules.

- Ignoring the holding period: The time you hold the units decides whether your gain is short-term or long-term.

- Forgetting the purchase date: Debt fund tax rules can change based on when you bought the units.

- Using one date for all SIP units: Every SIP instalment has its own purchase date and holding period.

- Assuming fund switching is tax-free: Moving money from one scheme to another counts as redemption and may create taxable gains.

- Paying tax on the full withdrawal: Tax usually applies to the profit, not the total amount you receive.

- Ignoring dividend income: Mutual fund dividends may be added to your taxable income.

- Confusing TDS with final tax: TDS is only an advance tax deduction. Your final tax may be higher or lower.

- Not reporting capital losses: Eligible losses may help reduce tax on capital gains.

- Using outdated tax rates: Mutual fund tax rules can change, so always check the latest rules.

- Not keeping proper records: Missing statements can make tax calculation and return filing difficult.

- Redeeming without tax planning: Check the holding period and possible tax before selling your mutual fund units.

No, you usually do not pay capital gains tax only because your fund value has increased. Tax normally applies when you sell or redeem the units at a profit. Dividend income may still be taxable when you receive it.

No, tax usually applies only to the profit earned from the investment. Your original invested amount does not count as a capital gain. The fund type and holding period decide the tax treatment.

Yes, every SIP instalment has its own purchase date and holding period. Older instalments may become long-term, while newer ones may remain short-term. Therefore, one redemption can include both types of gains.

Yes, a switch usually counts as selling units from one scheme and buying units in another. Any profit from the old scheme may become taxable. This rule may also apply when both schemes belong to the same fund house.

Reinvesting the money does not automatically remove the tax on your earlier gain. The redemption remains a separate taxable transaction. Tax-saving options depend on the latest rules and your personal situation.

Debt fund taxation rules have changed over time. Units purchased on different dates may follow different tax treatments. Always check the exact purchase date before calculating your tax.

The tax category depends on how much the fund invests in domestic equity and debt assets. Two hybrid funds can follow different tax rules even when their names sound similar. Check the scheme document or tax statement for the correct category.

Conclusion

So guys, in this article, we’ve covered Mutual Fund Taxation in detail. Understanding these tax rules can help you protect your returns and avoid common mistakes. I personally recommend checking the fund type, purchase date, and holding period before selling your units. You should also keep your investment statements safe for tax filing. Review your mutual fund portfolio today and plan your next redemption wisely.

The content on Finance Calculatorz is intended for educational and informational purposes. It provides general guidance on financial topics and tools. Readers are encouraged to use the information to make informed decisions about their finances.

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks