Direct vs Regular Mutual Funds – Choose Which is Better for You?

Published: 15 Jul 2026

Did you know that two people can invest in the same mutual fund and still earn different returns? The reason is the type of plan they choose. Direct and Regular mutual funds invest in the same portfolio, but they have different costs. Over time, even a small difference in fees can affect your final returns. In this guide, you’ll learn the difference between Direct and Regular mutual funds and find out which option may suit your investment goals.

1. What Is a Direct Mutual Fund?

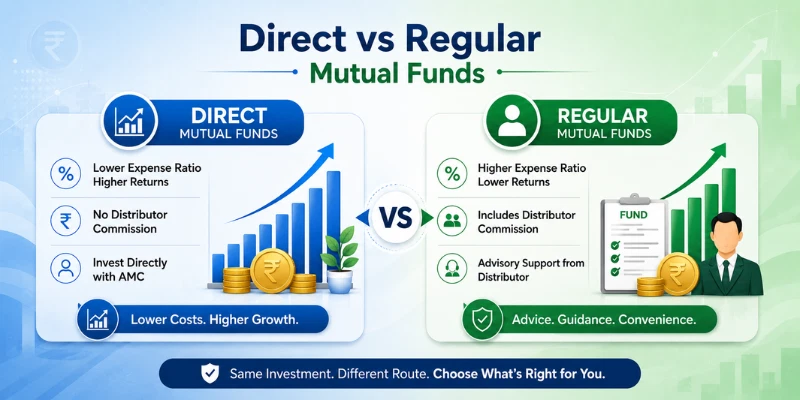

A Direct mutual fund is a plan that you buy directly from the asset management company (AMC) without using a broker or financial advisor. Since there is no middleman, you do not pay any distributor commission, which keeps the expense ratio lower. As a result, you may earn slightly higher returns over the long term compared to a Regular plan. However, you need to research and manage your investments on your own. When comparing Direct vs Regular mutual funds, a Direct plan is a good choice for investors who are confident in making their own investment decisions.

2. What Is a Regular Mutual Fund?

A Regular mutual fund is a plan that you buy through a broker, bank, or financial advisor who helps you choose and manage your investments. Because the advisor receives a commission, the expense ratio is slightly higher than a Direct plan. In return, you get professional guidance, which can be helpful if you are new to investing. This makes Regular plans a popular option for beginners and busy investors. In the Direct vs Regular mutual funds comparison, a Regular plan is best suited for those who value expert advice and convenience.

3. How Does a Direct Mutual Fund Work?

A Direct mutual fund works by allowing you to invest directly through the asset management company (AMC) without involving a broker or distributor. You can buy, redeem, or manage your investments using the AMC’s website or mobile app. Since there is no commission paid to a middleman, the expense ratio is lower, which can improve your long-term returns. You are responsible for selecting the right fund and tracking its performance. In the Direct vs Regular mutual funds comparison, Direct plans offer more control but require you to make your own investment decisions.

4. How Does a Regular Mutual Fund Work?

A Regular mutual fund works through a broker, bank, or financial advisor who acts as an intermediary between you and the AMC. The advisor helps you choose suitable funds, complete the investment process, and review your portfolio over time. For these services, the AMC pays the distributor a commission, which is included in the fund’s expense ratio. This makes investing easier, especially for beginners who need expert guidance. When comparing Direct vs Regular mutual funds, Regular plans offer convenience and professional support, but they usually come with slightly higher costs.

5. Features of a Direct Mutual Fund

A Direct mutual fund is designed for investors who prefer to manage their own investments. Since you invest directly with the asset management company (AMC), there is no distributor commission. This helps reduce costs and can improve your long-term returns. It is a suitable option for investors who have basic knowledge of mutual funds and are comfortable researching and monitoring their portfolios.

Key Features

- Lower expense ratio due to no distributor commission.

- Higher return potential over the long term.

- Purchased directly from the AMC’s website or app.

- No broker or financial advisor involved.

- Gives investors full control over investment decisions.

- Best suited for experienced and self-directed investors.

6. Features of a Regular Mutual Fund

A Regular mutual fund is a good choice for investors who want professional guidance throughout their investment journey. You invest through a broker, bank, or financial advisor who helps you choose suitable funds and manage your portfolio. Although the expense ratio is slightly higher because of the advisor’s commission, many investors find the expert support valuable.

Key Features

- Includes guidance from a broker or financial advisor.

- Easy to invest and manage for beginners.

- Higher expense ratio because of distributor commission.

- Available through banks, brokers, and investment platforms.

- Helps investors select funds based on their financial goals.

- Ideal for first-time investors and those who prefer expert assistance.

7. Direct vs Regular Mutual Funds: Comparison

Direct and Regular mutual funds invest in the same mutual fund scheme, but they differ in cost, support, and investment process. The main difference is that Direct plans do not involve any distributor, while Regular plans include the services of a broker or financial advisor. Your choice depends on your investment knowledge, time, and need for guidance.

1. What Is Expense Ratio?

The expense ratio is the annual fee charged by a mutual fund company for managing your investment. It covers the cost of fund management, administration, and other services. A lower expense ratio means more of your money stays invested, which can help improve your long-term returns.

2. Why Does Expense Ratio Matter?

- It directly affects your final investment returns.

- Direct mutual funds usually have a lower expense ratio.

- Regular mutual funds have a slightly higher expense ratio due to advisor commissions.

- Even a small difference in fees can create a big impact over many years.

Example

Suppose you invest ₹1 lakh in a mutual fund. A Direct plan with a 0.5% expense ratio will cost less than a Regular plan with a 1% expense ratio. Over 10–20 years, this small cost difference can reduce or increase your final wealth.

8. Benefits of Direct Mutual Funds

- Lower Costs: Direct mutual funds have a lower expense ratio because there is no distributor commission. This helps you save money over the long term.

- Higher Return Potential: Since the costs are lower, more of your money stays invested, which can help improve your overall returns.

- More Control: You can choose funds, track performance, and manage your investments without depending on an advisor.

- Greater Transparency: Direct plans clearly show the costs involved, helping you understand where your money is invested.

- Best for Self-Managed Investors: Direct mutual funds are suitable for people who have basic investment knowledge and can research funds on their own.

9. Drawbacks of Direct Mutual Funds

- No Expert Guidance: Direct mutual funds do not provide personal advice from a financial advisor, so you must make investment decisions yourself.

- Requires Research: You need to study different funds, compare options, and understand market conditions before investing.

- Higher Responsibility: Managing your portfolio, tracking performance, and making changes are completely your responsibility.

- Risk of Wrong Decisions: Without proper knowledge, you may choose unsuitable funds or make emotional decisions during market ups and downs.

- Not Ideal for Beginners: New investors who lack experience may find it difficult to select and manage funds without professional support.

10. Benefits of Regular Mutual Funds

- Expert Guidance: Regular mutual funds provide support from financial advisors who can help you choose suitable funds based on your goals and risk level.

- Easy Investment Process: Advisors handle many investment-related tasks, making the process simple for beginners.

- Better Decision Support: A financial advisor can help you avoid common mistakes and make better investment choices during market changes.

- Portfolio Monitoring: Advisors can review your investments and suggest changes when needed to keep you on track.

- Suitable for Beginners: Regular funds are a good option for investors who are new to mutual funds or do not have enough time to research and manage investments.

11. Drawbacks of Regular Mutual Funds

- Higher Costs: Regular mutual funds have a higher expense ratio because they include distributor or advisor commissions. This can reduce your long-term returns.

- Lower Return Potential: Since you pay extra fees for advice and services, your final returns may be slightly lower compared to Direct plans.

- Less Control: You depend on an advisor for fund selection and investment decisions, which may reduce your direct involvement.

- Quality of Advice May Vary: The support you receive depends on the knowledge and experience of your financial advisor.

- Not Always Cost-Effective: If you already understand mutual funds and can manage investments yourself, paying extra fees may not provide much value.

12. Direct vs Regular Mutual Funds: Which One Is Better?

The better option between Direct and Regular mutual funds depends on your investment knowledge, goals, and need for support. A Direct mutual fund may be better for investors who understand the market and can manage their investments independently. It has lower costs, which can help increase returns over the long term. On the other hand, a Regular mutual fund can be a better choice for beginners who need expert guidance and support.

1. Choose Direct Mutual Funds If:

- You understand how mutual funds work.

- You can research and select funds on your own.

- You want to reduce investment costs.

- You are comfortable managing your portfolio.

2. Choose Regular Mutual Funds If:

- You are new to mutual fund investing.

- You need help choosing the right funds.

- You prefer professional advice and support.

- You do not have enough time to track investments.

13. Tips to Choose Between Direct and Regular Mutual Funds

Choosing the right mutual fund plan depends on your knowledge, goals, and investment style. Before making a decision, understand your needs and compare both options carefully.

- Know Your Investment Knowledge: If you understand mutual funds and can research on your own, a Direct plan may be suitable. If you need guidance, a Regular plan can help.

- Compare Costs: Always check the expense ratio before investing. Lower costs can help you build more wealth over the long term.

- Set Clear Goals: Choose a plan based on your financial goals, such as buying a home, saving for retirement, or building wealth.

- Avoid Following Others: Do not choose a plan just because your friends or family are investing in it. Select an option that matches your needs.

- Review Your Investment Regularly: Keep track of your portfolio and make changes when needed to stay on the right path.

Yes, you can switch from a Regular plan to a Direct plan of the same mutual fund scheme. However, the switch may be treated as a redemption and a new investment, which can have tax or exit load effects. Always check the charges before making a switch.

Yes, both plans invest in the same portfolio and are managed by the same fund manager. The main difference is the cost and the way you invest. The returns can differ because Direct plans have lower expenses.

No, Direct and Regular mutual funds have the same market risk because they invest in the same assets. The difference is that Direct plans require you to manage your investment decisions yourself. Your risk depends more on the fund type you choose, not the plan type.

A financial advisor can be useful if you need help choosing funds and managing your investments. Their guidance can help beginners avoid common mistakes. However, experienced investors may prefer Direct plans to save on extra costs.

Even a small difference in expense ratio can impact your final returns over many years. This happens because the saved amount also gets the benefit of compounding. Long-term investors should always consider costs before investing.

Beginners should choose based on their confidence and understanding of investing. If you need support and want someone to guide you, a Regular plan can be helpful. If you are willing to learn and manage investments yourself, a Direct plan can be considered.

Conclusion

So guys, in this article, we’ve covered Direct vs Regular mutual funds in detail. Both plans have their own benefits, and the right choice depends on your knowledge and investment needs. In my opinion, Direct plans are better for investors who can manage their investments, while Regular plans work well for those who need expert guidance. Choose wisely based on your goals and comfort level. Start investing today and take a step toward building your financial future.

The content on Finance Calculatorz is intended for educational and informational purposes. It provides general guidance on financial topics and tools. Readers are encouraged to use the information to make informed decisions about their finances.

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks