Pros and Cons of Mutual Funds which you should know

Published: 6 Mar 2026

Have you ever wanted to grow your money but felt too scared to start? You are not alone. The stock market can feel confusing with thousands of companies to pick from. It is easy to feel stuck and do nothing.

That is where mutual funds come in. Before you invest, you need to understand the pros and cons of mutual fund. Think of a mutual fund like a potluck dinner. At a potluck, everyone brings one dish. Together, you have a full meal and get to taste a little bit of everything. A mutual fund works the same way. Many people put their money together, and that pool of money buys a little bit of many different companies.

But are mutual fund right for you? In this guide, we will look at both sides. You will learn the pros and cons of mutual funds in plain language. By the end, you will know if they fit your money goals. Let us dive into the pros and cons of mutual funds together.

1. What Exactly is a Mutual Fund?

Before we explore the pros and cons of mutual funds, let us make sure we understand what they are. A mutual fund is a company that gathers money from many people. Then, it uses that money to buy different investments like stocks, bonds, or other assets.

A professional person called a fund manager makes the choices about what to buy and what to sell. When you put money in a mutual fund, you buy shares. Each share represents a small piece of everything the fund owns.

Here is a simple example to make it clear. Imagine you have $100. You cannot buy one share of Amazon, Google, and Microsoft because they cost too much individually. But a mutual fund can buy all three. Your $100 gives you a tiny slice of all those big companies. This is the basic idea behind how mutual fund work. Now let us examine the pros and cons of mutual funds in detail.

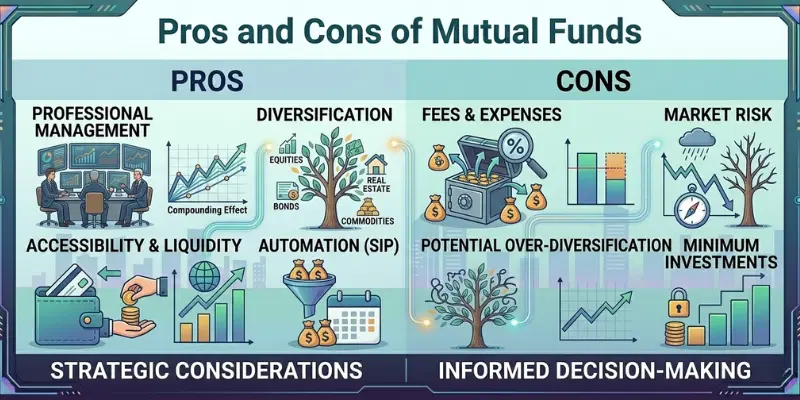

2. The Advantages of Mutual Funds

Many people love mutual funds, and for good reason. Let me explain the main advantages. Understanding the pros and cons of mutual fund means looking at both benefits and drawbacks.

1. You Do Not Need to Be an Expert

Do you know how to pick winning stocks? Most people do not, and that is completely okay. When you use a mutual fund, a professional does the work for you. This is one of the biggest pros of mutual funds. The fund manager studies companies all day. They read reports, watch the news, and know the numbers inside and out.

Think about fixing your car. You could watch YouTube videos and try to do it yourself, but it is easier and safer to take it to a mechanic who knows what to do. A fund manager is like that mechanic. They handle the hard work so you do not have to worry about it.

2. You Can Start with Small Money

Some investments need a lot of cash to begin. Buying individual stocks can cost hundreds or even thousands per share. But many mutual funds let you start with a small amount. This advantage makes the pros and cons of mutual funds lean positive for beginners. Some funds let you begin with just $50 or $100. You can even set up automatic investments where you put $25 from every paycheck into a fund. Over time, that small money can grow into something big without you feeling the pinch.

3. Your Money Gets Spread Out

There is an old saying: “Do not put all your eggs in one basket.” If you drop the basket, all your eggs break. The same is true with money. If you buy stock in just one company and that company does badly, you lose money. But a mutual fund owns many companies. If one company drops, others might go up. This balance helps protect you from big losses.

Here is a real-life example. Imagine you own a small store. If you only sell ice cream, you do well in summer. But in winter, your sales drop. If you also sell hot coffee, you make money all year round. A mutual fund does the same thing by mixing different types of investments to smooth out the ups and downs.

4. It is Easy to Get Your Money

Some investments are hard to sell quickly. Real estate is a good example. If you need cash fast, you cannot sell a house in one day. Mutual funds are different. You can sell your shares on any business day, and the money usually shows up in your bank account in a few days. This makes mutual fund a good choice if you think you might need the money later for something important.

5. You Do Not Need to Watch It Every Day

Stocks can go up and down every minute, and watching this can be stressful. With mutual funds, you do not need to check every day. You can relax and let the manager handle it. This is great for people with busy lives who do not have time to follow the market constantly.

6. Your Money Can Grow in Different Ways

Mutual funds can make money in two ways. First, the companies in the fund might pay dividends, which are small payments of profit. The fund sends this cash to you automatically. Second, the value of the fund can go up. If the companies do well, your shares become worth more. Over many years, this growth can add up significantly through the power of compounding.

To sum up the advantages side of the pros and cons of mutual fund:

- You get professional management without needing to be an expert yourself

- You can start investing with small amounts of money

- Your risk is spread across many different companies

- You can access your money quickly when you need it

- You do not need to watch the market every single day

- Your money can grow through both dividends and price increases

These pros of mutual funds make them attractive to millions of investors worldwide.

3. The Disadvantages of Mutual Funds

Mutual funds are not perfect. They have some downsides you need to know about before you invest. Looking at the complete pros and cons of mutual funds means understanding the drawbacks too.

1. You Have to Pay Fees

Nothing in life is free, and mutual funds are no different. The fund manager and the company need to get paid for their work. They charge fees that come out of the fund’s money, which means less profit for you in the end. This is one of the main cons of mutual funds. The main fee is called the expense ratio, and it is shown as a percentage. For example, a 1% expense ratio means you pay $1 per year for every $100 you have in the fund. Some funds charge high fees while others charge low fees. Over many years, high fees can eat up a lot of your profits, so it pays to look for funds with low expense ratios.

2. You Do Not Control the Choices

When you buy a mutual fund, you give up control over where your money goes. The fund manager decides what to buy and sell. You cannot tell them, “Please do not invest in that company.” You have to trust their judgment completely. For some people, this feels fine and even relaxing. For others, it feels uncomfortable not having a say. Ask yourself whether you are okay with letting someone else make the big decisions about your money.

3. Your Money Can Still Lose Value

Mutual fund are not a guarantee of profits. They are investments, and all investments have risk. The stock market goes up and down, and some years it drops a lot. In 2008, many mutual funds lost a lot of value during the financial crisis. People who needed their money that year had to sell at a loss. When weighing the pros and cons of mutual funds, remember they are safer than buying one single stock, but they are not as safe as keeping money in a bank account with FDIC insurance.

4. You Might Pay Taxes on Gains

Even if you do not sell your shares, you might owe taxes each year. When the fund manager sells investments that went up in value, that is called a capital gain. The fund passes these gains to you, and you have to pay taxes on them. This can be a surprise for new investors who do not expect a tax bill from an investment they still own. It is important to understand this before you invest in a taxable account.

5. There Are Too Many Choices

This sounds like a good thing, but it can actually be a problem. There are thousands of mutual fund out there. How do you possibly pick the right one? Some focus on big companies, some on small companies, some on other countries, and some on bonds instead of stocks. Too many choices can freeze you, and you might end up not picking any fund at all. This is called analysis paralysis, and it stops many people from starting to invest.

6. You Might Not Beat the Market

Many mutual funds try to “beat the market” by doing better than the average stock market return. But most funds do not succeed in the long run. Studies show that over many years, most funds actually do worse than the overall market. After you pay the fees, your returns are often lower than a simple index fund that just tracks the market. This is a big disadvantage when examining the pros and cons of mutual funds.

Here are the main disadvantages side of the pros and cons of mutual fund:

- You pay fees that reduce your overall profits over time

- You give up control of investment decisions to someone else

- Your money can still lose value when the market drops

- You may owe taxes on gains even if you did not sell anything

- The huge number of choices can be overwhelming

- Most funds do not beat the simple market average after fees

These cons of mutual funds are important to know before you invest your hard-earned money.

4. Real-Life Example: Two Friends, Two Choices

Let me tell you about two friends to make these ideas clearer. Their names are Mike and John, and they both wanted to grow their money. Their stories show the real-world pros and cons of mutual fund in action.

Mike decided to keep things simple. He picked one mutual fund that owns the 500 biggest US companies. He put $200 in every single month without fail. He did not worry about the daily ups and downs in the market. He just kept investing consistently. After 15 years, his money had grown a lot thanks to the power of compounding and steady investing.

John took a different path. He wanted to pick his own stocks. He bought three companies he liked after doing some research. One company did really well and doubled in value. One company stayed flat and did nothing much. One company went out of business completely. After 15 years, John had less money than Mike even though they both started with the same amount.

What can we learn from Mike and John? Mike used the advantages of mutual funds wisely. He kept it simple, stayed patient, and let the professionals handle the details. John took big risks by putting all his hope in just three companies. This comparison highlights the pros and cons of mutual funds versus individual stock picking. For most regular people, mutual funds offer a simpler and safer path to growing wealth over time.

5. Tips for Beginners to Get Started

If you want to try mutual funds after learning about the pros and cons of mutual funds, here are some practical steps to follow. These tips will help you avoid common mistakes and start on the right foot.

Start with an index fund: An index fund is a special type of mutual fund that simply tracks a market index like the S&P 500. It does not try to beat the market or pick winning stocks. It just tries to match the market’s performance. These fund have very low fees because they do not need expensive managers making active choices. They are a great place for beginners to start without getting overwhelmed.

Reinvest your earnings automatically: When the fund pays you dividends, use them to buy more shares. This is called reinvesting, and most funds let you do it automatically. Over time, this can make a huge difference in your final returns. Your money starts earning money on itself, and it grows faster and faster like a snowball rolling downhill.

Be patient for the long term: Mutual funds work best over long periods of time. Think 5 years, 10 years, or even more. Do not panic when the market drops temporarily because it always goes up again over time. If you sell when prices are low, you lock in your losses and miss out on the recovery. Patience is the secret ingredient to successful investing.

Watch the fees carefully: Before you buy any fund, check the expense ratio in the fund’s information. Try to find funds with fees under 0.50% if possible. Remember that lower fees mean more money stays in your pocket to grow over the years. Even a 1% difference in fees can cost you tens of thousands of dollars over a lifetime of investing.

Spread your money around: Do not put all your money in one type of fund. Maybe pick one US stock fund and one international fund to add more balance. You could also add a bond fund if you want less risk. This diversification helps protect you no matter what happens in any single market.

Here is a quick checklist for beginners who have considered the pros and cons of mutual fund:

- Open an account with a low-cost broker like Vanguard, Fidelity, or Charles Schwab

- Choose one simple index fund that tracks the whole US market

- Set up automatic monthly investments so you do not have to think about it

- Reinvest all dividends to buy more shares

- Ignore the news and do not check your balance every day

- Stay invested for at least five years without touching the money

You need to open an account with a brokerage company first. Popular choices include Vanguard, Fidelity, Charles Schwab, or even apps like Robinhood. Once your account is funded, search for the mutual fund you want, enter the amount, and click buy. It is very similar to shopping online.

Active funds have a manager who tries to pick winning stocks to beat the market. Index funds simply copy a market index like the S&P 500 and do not try to beat it. Index funds have much lower fees and actually perform better than most active funds over time.

Yes, your account value will drop if the market crashes. But you only lose money permanently if you sell when prices are low. If you stay invested, the market has always recovered and grown over time. That is why mutual funds are for long-term goals, not short-term needs.

Start with a low-cost index fund that tracks the S&P 500. This type of fund simply follows the 500 biggest US companies. It gives you instant diversification without needing to pick winning funds. Look for words like “Index Fund” or “S&P 500” in the name, and check that the expense ratio is under 0.10%.

You can start with as little as $50 to $100 with many fund companies. Some funds have no minimum at all if you agree to invest small amounts monthly. The important thing is to start something, even if it is small, and build the habit.

You may owe taxes each year even if you did not sell any shares. When the fund manager sells stocks for a profit, that profit passes to you as a capital gain. These gains are taxable. To avoid surprises, you can hold mutual funds in tax-advantaged accounts like IRAs or 401(k)s.

The biggest mistake is panic selling when the market drops. Many beginners see their account value go down and sell in fear. This locks in their losses and makes them miss the recovery. The second biggest mistake is ignoring fees, which quietly eat away returns over many years.

Conclusion

So guys, in this article, we’ve covered the pros and cons of mutual funds in detail. Here is my personal take on it. I believe mutual funds are one of the best options for regular people who want to grow their money without stress. The key is to keep it simple. Start with a low-cost index fund, invest every month, and do not panic when the market drops. That simple plan has worked for millions of people over many decades.

Your turn now. What is the biggest thing stopping you from investing in mutual funds? Is it fear, confusion, or something else? Let me know in the comments. I read every reply and would love to help.

The content on Finance Calculatorz is intended for educational and informational purposes. It provides general guidance on financial topics and tools. Readers are encouraged to use the information to make informed decisions about their finances.

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks