Step-by-Step Working of Mutual Funds

Published: 3 Mar 2026

Mutual funds have made investing simple and accessible for millions of people. But many beginners still feel confused about what happens to their money after they invest. Where does the money go? Who manages it? And how does it grow over time? Understanding the working of mutual funds answers these important questions and helps you invest with confidence. When you know how the process works, you can make smarter decisions and stay calm during market changes. In this article, you will learn how mutual funds operate step by step in a clear and simple way.

1. What Is Mutual Funds?

A mutual funds is a pooled investment vehicle where money from many investors is collected and invested in different assets like stocks, bonds, or other securities. Instead of investing alone, you invest together with others. This pooled money is managed by a professional fund manager who makes investment decisions on behalf of all investors.

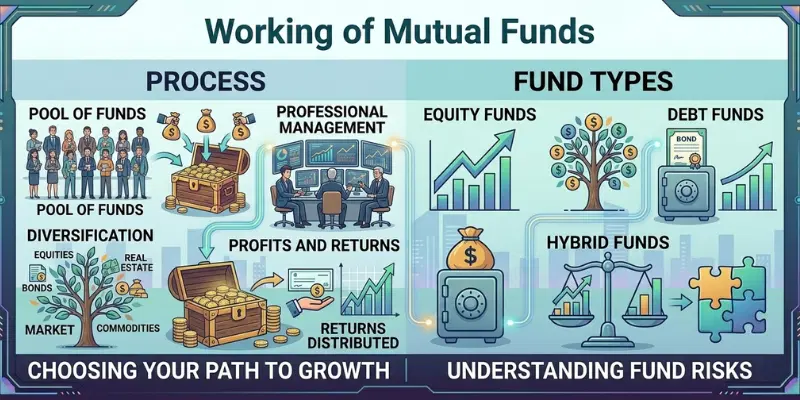

2. How Mutual Funds Work

Mutual funds operate by pooling money from many investors and investing it in a mix of assets to generate returns. The goal is to grow your money over time while reducing risk through diversification. Instead of managing investments yourself, a professional funds manager makes the key decisions. Understanding the step-by-step working of mutual funds helps you invest confidently and avoid confusion.

1. Pooling of Money

When investors put their money into a mutual fund, all contributions are collected together into a single investment pool. This collective approach allows even small investors to access big opportunities in the stock and bond markets. The funds becomes powerful because it can invest in multiple assets that would be hard to reach individually. Each investor owns units of the fund, representing their share of the total investment pool.

2. Allocation of Funds

After pooling, the funds manager decides how to invest the money based on the fund’s objectives. equity funds are focused mainly on stocks, debt funds on bonds and fixed-income securities, and hybrid funds combine both. The manager carefully distributes the money to balance potential returns with acceptable risk levels. Proper allocation ensures that investors can achieve their financial goals without taking unnecessary risks.

3. Units and NAV

Each investor gets “units” of the mutual fund based on their contribution. The price of a single unit is called the NAV, which is calculated daily. NAV equals the total value of all fund assets minus liabilities, divided by the total number of units. As the value of the underlying investments rises or falls, the nav changes, directly affecting the value of your investment.

4. Generating Returns

Mutual funds generate returns mainly through two sources: capital appreciation and income. Capital appreciation happens when the value of the fund’s investments increases over time. Income is earned from dividends on stocks or interest from bonds held by the fund. These returns are then reflected in the NAV, increasing the value of each unit for investors.

5. Redemption Process

Investors can redeem, or sell, their units back to the mutual fund whenever they need money, especially in open-ended funds. The amount you receive depends on the current NAV of the fund units at the time of redemption. This process is simple and provides liquidity, allowing you to access your investment easily. Redemption ensures that investors can exit without waiting for a fixed maturity period, depending on the funds type.

3. Role of Key Participants in Mutual Funds

Mutual funds work smoothly because of several key participants who manage, safeguard, and oversee the investment process. Each participant has a specific role that ensures your money is invested efficiently and securely. Understanding these roles helps investors know who is responsible for what and why professional management adds value.

1. Fund Manager

The fund manager is the brain behind all investment decisions. They research the market, select stocks, bonds, or other assets, and decide how to allocate the pooled money. Their goal is to maximize returns while managing risk according to the fund’s objectives. A skilled fund manager can make a big difference in the growth of your investment over time.

2. Asset Management Company

The AMC is the organization that creates and runs the mutual funds. It handles administrative tasks, regulatory compliance, and overall management of the funds. The AMC hires fund managers, ensures proper record-keeping, and maintains investor communications. Essentially, it provides the structure and support needed for the fund to operate efficiently.

3. Custodian

The custodian is responsible for safekeeping the fund’s securities, such as stocks and bonds. They make sure all assets are protected and properly accounted for. The custodian also handles settlement of transactions and ensures compliance with regulations. This role ensures the investor’s money is secure and properly managed.

4. Investors

Investors provide the capital that fuels the mutual funds. They buy units of the fund, earn returns based on performance, and have the flexibility to redeem their units when needed. Investors’ collective contributions make it possible to access large and diverse markets that would be difficult individually.

4. Expenses and Charges in Mutual Funds

While mutual funds help your money grow, they also come with certain costs. These expenses pay for professional management, operational work, and other services that make investing easier for you. Understanding these charges is important because they can slightly reduce your overall returns if ignored.

1. Expense Ratio

The expense ratio is the annual fee charged by the fund to manage your investment. It covers fund management, administrative costs, and other operational expenses. This fee is deducted directly from the fund’s assets, so you don’t pay it separately. Lower expense ratios are generally better because they leave more of your money to grow.

2. Management Fees

Management fees are part of the expense ratio but specifically compensate the fund manager for their expertise. Skilled fund managers analyze markets, select investments, and make strategic decisions. While you pay for this professional service, it can significantly impact the fund’s performance over time.

3. Entry and Exit Loads

Some mutual funds charge a small fee when you buy (entry load) or sell (exit load) units. Entry loads are rare today, but exit loads may apply if you withdraw your money before a specified period. This encourages long-term investing and discourages short-term trading that could affect the fund’s stability.

Example

If you invest $10,000 in a fund with a 1% expense ratio, $100 per year is used to cover fund expenses. The remaining $9,900 continues to grow in the market. Over time, even small differences in expense ratios can add up, making it important to choose cost-effective funds.

5. Real-Life Example: How Mutual Funds Work in Real Life

Understanding mutual funds becomes much easier with a practical example. Let’s break it down step by step to see how your money grows when invested in a mutual fund.

Step 1: Pooling of Money

- Suppose 100 investors decide to invest $1,000 each.

- The total pooled amount becomes $100,000.

- This pooled fund allows the manager to access bigger and diversified investment opportunities than individual investors could on their own.

Step 2: Investment by Fund Manager

- The fund manager invests the pooled money according to the fund’s objective.

- For example, the fund may allocate:

- 70% to stocks for growth

- 30% to bonds for stability and steady income

- This allocation helps balance risk and return for all investors.

Step 3: Growth of Investment

- Over the year, the stocks perform well, and the bonds provide interest income.

- The total value of the fund rises from $100,000 to $120,000.

- This increase is reflected in the net asset value (NAV), which is the price of one unit of the fund.

Step 4: Returns to Investors

- Let’s say you initially invested $1,000 and received 10 units at an NAV of $100.

- After growth, the NAV rises to $120.

- Your 10 units are now worth $1,200.

- You earned a profit of $200 without needing to buy or sell individual stocks yourself.

Mutual funds generate returns through capital appreciation and income from dividends or interest. When the value of stocks or bonds in the fund rises, your investment grows. Returns are reflected in the NAV, which changes daily based on market performance.

NAV (Net Asset Value) is the price of one unit of the mutual funds. It represents the total value of all assets minus liabilities, divided by the number of units. NAV helps determine how much your investment is worth at any time.

A professional fund manager, hired by the Asset Management Company (AMC), manages the fund. They research the market, select investments, and balance risk and return. Their expertise helps investors grow money without handling day-to-day market decisions.

Yes, mutual fund investments are subject to market risks, and NAV can go down temporarily. However, diversification reduces risk compared to investing in a single stock. Long-term investing usually smooths out short-term fluctuations and increases the chance of growth.

You can invest directly through the AMC or via online platforms and brokers. Choose a fund that matches your goal, risk tolerance, and time horizon. You can start with a lump sum or regular SIPs depending on your preference.

Investors provide the capital that the fund invests in various assets. They earn returns based on the fund’s performance and can redeem their units when needed. Investors’ money enables the fund to pool resources and access larger investment opportunities.

NAV is calculated daily for most open-ended mutual funds. It reflects the current value of the fund’s underlying investments. Regular updates help investors know the exact worth of their investment at any time.

Conclusion

So guys, in this article, we’ve covered Working of Mutual Funds in detail. Understanding how your money is pooled, invested, and managed helps you make smarter decisions and stay calm during market fluctuations. My personal recommendation is to start with a simple open-ended or hybrid fund while learning the basics. Begin your investment journey today and take control of your financial future.

The content on Finance Calculatorz is intended for educational and informational purposes. It provides general guidance on financial topics and tools. Readers are encouraged to use the information to make informed decisions about their finances.

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks